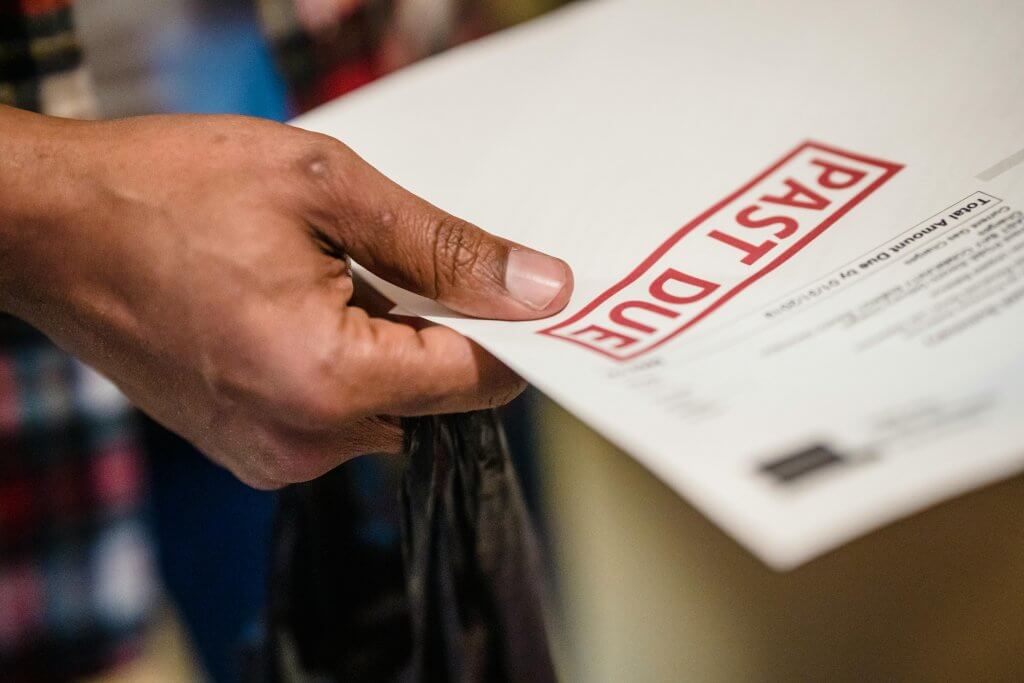

If you’re asking the question ‘is my business approaching insolvency?’ now is a good time to take stock of your company’s situation.

How are you coping? Are you well-placed to be able to deal with what the next 6-12 months holds? Will you have a viable business this time next year?

And, importantly, what are the signs that indicate all is not well with your business? This is a process of questioning we go through with many of our clients before deciding on the best course of action to take to save their business. We hope that by following these practical steps, we can help you tackle your own business’ challenges.

So what do you know about partnerships, how they work and the benefits they can bring? This article will explain all.

Taking stock

It’s very easy to find an excuse for putting off ‘auditing’ your business. After all, there is the day-to-day running of the business to take care of.

But this is not the time to vacillate. Remember, the sooner you know where you stand, the sooner you can devise an action plan, a strategy to take your business forward.

And if you do find the figures are not looking good, then the sooner you can employ the services of a business rescue specialist. Their expertise and experience will be invaluable as you steady the ship and plot a forward course.

So what should you be looking for? Here are some indicators that all is not well.

Tell-tale signs of a struggling business insolvency

When you analyse your business there are some tell-tale signs of business insolvency. These include:

1. Poor sales and an empty (or depleted) order book

This could mean you have to radically re-engineer your business. Ask yourself the following question: are you producing the right goods or services for today’s marketplace? That is, are you giving your customers what they really need?

Look at what your competitors are doing. Check out their prices, their customer service levels, and any ancillary services they offer. What are they doing better than you?

It could be that they have a more switched-on sales team, more imaginative marketing, a comprehensive and easy-to-use website, and are easily contactable so that potential clients can find the right point of contact to get the information they require.

Look at your sales and marketing team(s). Are the right people in the right positions? Are the correct processes in place, regarding sales targets, customer relationship management systems, and management of staff, including training? Are the more senior staff in the department(s) accountable? Would the appointment of new team members, or new management, be beneficial or detrimental to the way they work?

More drastically, have you considered outsourcing these functions? Working with a specialist agency could help you re-focus the business. A fresh pair of eyes can help rejuvenate a business that has been stuck in a rut (it happens to many, many businesses).

2. Heavy borrowing

This might not be as bad as it first sounds – so long as you and your financial director are in control. This is where your cash flow forecasting skills will be tested to the full.

Many firms have taken on large loans to help them survive the pandemic (including via various government support schemes). The key to paying them back is to have a realistic, informal repayment schedule that you can agree with your creditors.

Do base this repayment schedule on your expected income and don’t over-promise. If you let your creditors down during the term of an informal arrangement they may not be so sympathetic to your plight and may insist on a more formal arrangement going forward.

Importantly, before you talk to your creditors speak to a business rescue specialist. We can help advise you on setting up an informal arrangement that avoids going through the courts, and so saving you time, money and stress.

Of course, if the debt repayment schedule looks beyond your means, then you may be facing insolvency (or may already be insolvent). You must act fast in this circumstance: contact a licensed insolvency practitioner (IP) at once. They will explain the options available to you, and steer you through the whole process, whichever route you choose to take.

3. Late payment of suppliers or the refusal of suppliers to supply goods/services

The first of these frequently leads to the second, which is likely to be a critical issue for your business. To make matters worse, in some sectors a company will rely on a great many different suppliers, especially in the manufacturing, retail, hospitality and travel industries, making it hard to juggle payments when cash is tight.

The key here is good communication. If you find you’re financially ‘embarrassed’, speak to your suppliers and be honest. They are likely to be sympathetic, especially if you have a long-established relationship, and you have previously had a good ‘credit history’ with them.

Just about the worst thing you can do is to keep them in the dark. If you are not open with them then your relationship will be put under strain, and might even fracture.

If they refuse to supply you with goods and services you can always seek alternative suppliers (although the debt you owe them won’t go away). However, a new supplier will probably insist on stricter credit terms than you have had before, and may even ask for money upfront before they will work with you.

4. Late or non-payment of staff wages

Again, this is a sign that your business is in serious trouble. Aside from the moral issues – the distress and hardship the non-payment of wages can bring – you risk losing key members of staff (possibly to your competitors).

Distressed businesses are rarely happy places to work. Employees will soon start looking for other jobs. And while a reduction in headcount might be one of the things the business actually needs, it’s far better for the business if you are in control of the situation.

However, the bottom line is this: if you can’t pay your employers then there is a very possibility that you are facing insolvency.

5. Non-payment of cash owed to HMRC

One of the first signs of financial distress can be when that ‘nasty’ letter from HMRC lands in the in-tray. It is notoriously tough when it comes to unpaid debts. HMRC has significant resources it can employ against debtors – and it rarely hesitates to use them. It is a major driver of firms being wound-up through the courts.

In fairness, it does offer solutions to struggling businesses. Among other things the deferral of VAT payments and ‘time-to-pay’ tax arrangements are in place.

When dealing with HMRC take advice from your accountant or another financial or business specialist. They are paid to deal with these issues and understand the wisest approach to take when dealing with them.

6. Directors putting their own money into the business

How serious this indicator is as a sign of business insolvency depends on two things: how much and how often.

Continually using your own money to ‘bail out’ the company is a red flag, as is regularly using your personal credit cards for business activity. So too is not paying yourself.

If any of the scenarios listed above happen only occasionally, and the money is paid (or returned) to you, the chances are you have issues with your cash flow.

This could have serious consequences, so if you haven’t got the in-house expertise to deal with the situation then employ the services of a business rescue expert to help you.

Conversely, if they are regular occurrences then it may mean you are only putting off the inevitable, and the chances are your business is insolvent. At this point you need specialist advice from a licensed insolvency practitioner.

What can you do?

If you (and your fellow directors or co-owners) have decided that your business has no future, then you need to employ the services of an insolvency expert who will guide you through the options available as you take the formal insolvency route.

However, should you decide to carry on, you need to take immediate action to shore up your finances. Again, a specialist business recovery expert will be invaluable in helping you do this.

The most important thing you can do at this stage is to take control of the business. This involves scrutinizing every aspect of the business with a view to:

Cutting cost & overheads:

Are your departments & teams working to maximum efficiency? Are you making the most of up-to-date technology, including software?

Re-negotiating with suppliers:

Are you getting the best prices? When did you last seek alternative sources of supply? If you have a good relationship with your current suppliers, they might be amenable to offering you discounts (perhaps on a short-term basis) in order to keep your businesses longer term. You need to explore all of the above to save money and make your business viable going forward.

Analysing your staffing needs:

If you have been struggling for a while the chances are that you’ve already made staff redundant, and this may be an area where there is no more fat left to cut. However, if you’ve taken advantage of the furlough scheme it may be that you have staff who are returning to work.

And with the furlough scheme being wound down, can you afford to pay them? Perhaps they might agree to taking a pay cut in exchange for more holiday, a shorter working day, or part-time or flexible working arrangements?

One outcome of the pandemic has been the speeding up of the transition to home working, so work out who could work from home efficiently (perhaps coming into the workplace once or twice a week or when they are needed). This is a difficult area so tread cautiously.

Talk to your staff about what they want and what suits them, so you can come to a suitable arrangement amicably. Remember, everyone is different, and what works for one person might not work for another.

Reducing the wage bill:

Look in the mirror – are you getting a fair pay packet? Are you paying yourself (and your fellow directors) bonuses? Cutting your own remuneration could help the business short-term and will send out the message to staff that ‘you are all in it together’.

Sorting out underperforming departments:

Are the various departments that constitute your business fit for purpose? If they are not, the task of analysing why is not an easy one. Is it that staff members are underperforming? Or that the way the department works is outdated, and processes need updating and streamlining.

Underperformance of individual staff members is a difficult thing to deal with. The key here is not to be confrontational. Instead, try to be understanding, helping the employee who may be struggling either at work or outside of work. It may be, however, that problems are too deep-rooted, and go beyond the performance of individual staff members.

In this case, why not consider outsourcing their function to a specialist firm? This might be the most cost-effective and efficient way of going forward, so do some research into potential businesses with which you could partner.

Where you uncover the problems listed above, it’s important you analyse them so you can get to the root causes. These problems are bound to get worse over time if you don’t put steps in place to deal with them.

Many company owners and directors will be struggling to cope with the impact of the pandemic. Now’s the time to take an honest approach. Can the business ride out the current ‘rough patch’, or is it altogether more serious?

Whichever is the case, you need to act immediately. If it is the worst-case scenario, then you need to put in place insolvency arrangements with the help of a licensed insolvency practitioner.

While financial distress is a difficult topic to discuss, early intervention from a business rescue expert can help save a company.

Also remember that if your company is insolvent you, as a company director, have a legal duty to put the interests of creditors ahead of all other interests.

By recognising the early signs of business insolvency and seeking advice, we can give you the chance to turn things around. Contact our team of licensed insolvency practitioners and business rescue experts.